"The hotel segment bounces back to full pre-pandemic strength"

José Luis García-Hirschfeld

Hotels. Capital Marketsjoseluis.garciah@savills.es

Hotels. Capital Marketsjoseluis.garciah@savills.es

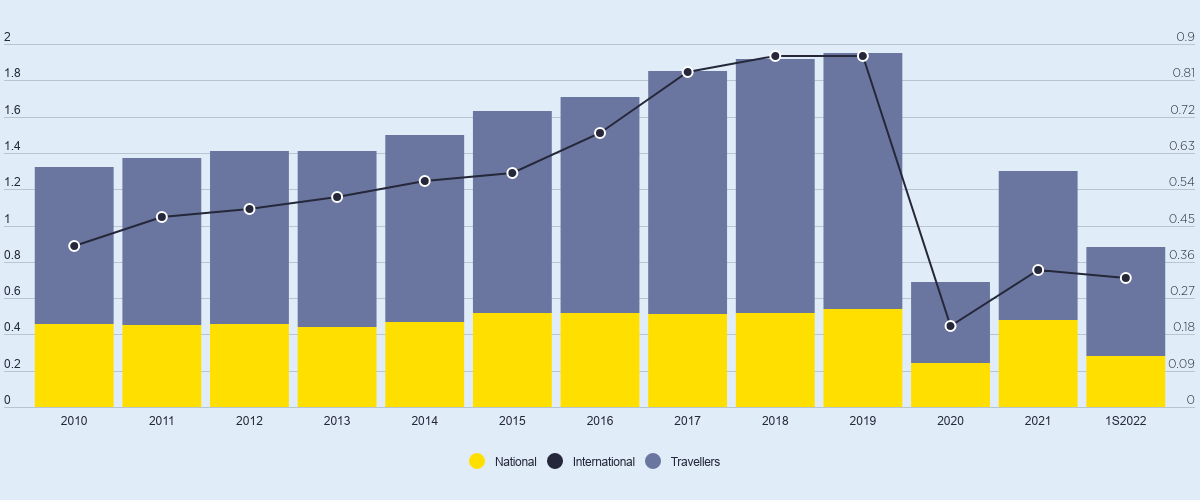

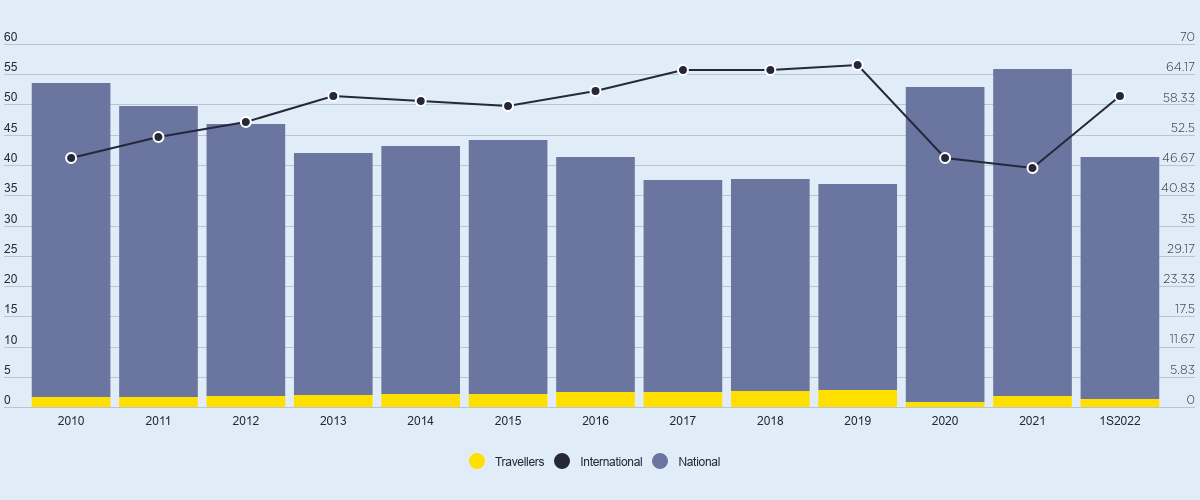

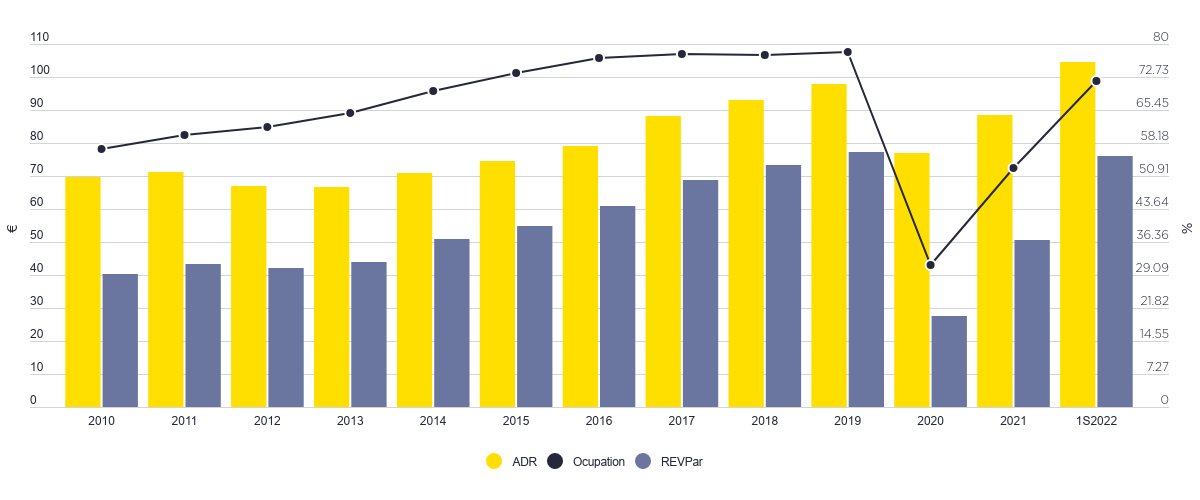

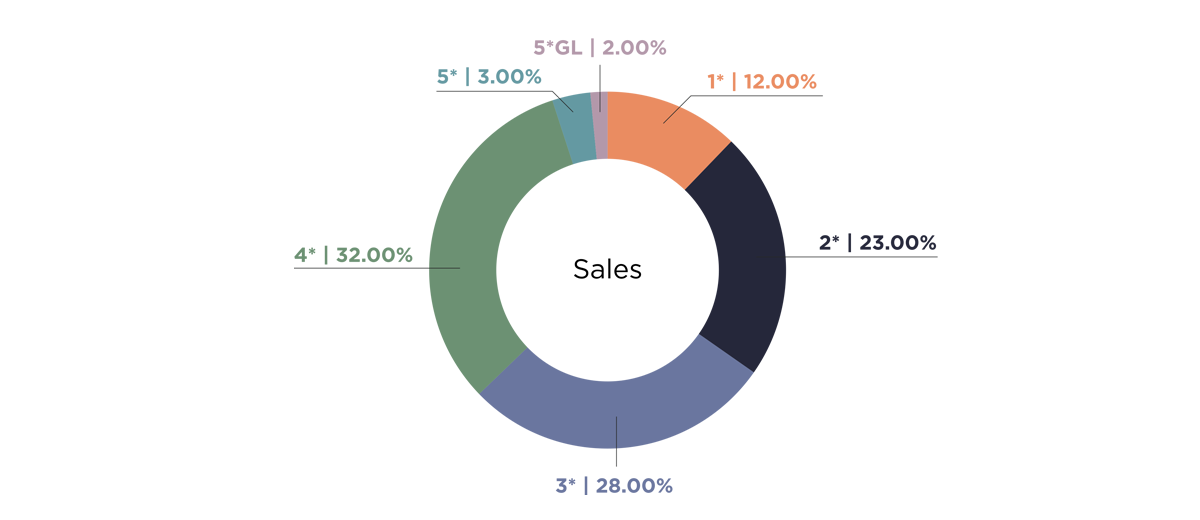

In the last two years, more than 2,000 beds have been added to the capital's hotel stock. We have gone from approximately 12,250 rooms in 2019 to 14,270 in 2021, a figure which, however, still ranks the city behind the hotel capacity of the capitals of Seville and Granada, with 25,670 and 15,970 rooms respectively. During the last year, four hotels have opened in Malaga city, all of them 4* and 5*. The range of hotel offerings is evolving in terms of quantity and quality. But for the moment, the 5* and Grand Luxury category accounts for only 5%, compared to 35% for 1* and 2* hotels. This proportion will be offset in time by the opening of new projects, which will add more than 1,500 4* and 5* rooms over the next few years. In addition, new accommodation formats are arriving, such as hostels and co-living. The occupancy and average price data are positive. We expect to close 2022 with occupancies of around 78.3%, very similar to 2019 (77%), and with an ADR approximately 7% higher, after reaching €104.50 in the first half of 2022. When compared with the municipalities of Marbella or Estepona, where the Revpar in August of this year has exceeded €236 and €249, respectively, it is clear how far the capital city has progressed. Investors and operators continue to look for assets to transform into hotels, hostels, tourist flats and other types of accommodation in Malaga city. The prospects for price increases and improved occupancy allow us to move forward despite rising costs due to inflation, so we remain in a market where demand is high and the supply of properties in good locations is low.